Результаты для "ar(1) model"

Авторегрессионная модель - Википедия

https://ru.wikipedia.org/wiki/%D0%90%D0%B2%D1%8...

Авторегрессионная (AR-) модель (англ. autoregressive model) — модель временных рядов, в которой значения временного ряда в данный момент линейно зависят от ...

Autoregressive model - Wikipedia

https://en.wikipedia.org/wiki/Autoregressive_model

In statistics, econometrics, and signal processing, an autoregressive (AR) model is a representation of a type of random process; as such, it can be used to ...

Авторегрессия (AR, autoregression) - Forecast NOW!

https://fnow.ru/algorithm-comparison/avtoregressia

Рисунок 1б. Авторегрессия, порядок модели p = 1. Как можно видеть из рисунка 1б и 2 низкий порядок авторегрессии ...

autoregressive linear models ar(1) models - Stat@Duke

https://www2.stat.duke.edu/courses/Spring00/sta...

The zero-mean AR(1) model xt = xt 1 + t is a linear regression of the current value of the time series on the previous value.

Autoregressive (AR) Model for Time Series Forecasting

https://www.geeksforgeeks.org/data-analysis/aut...

23 июл. 2025 г. ... Autoregressive models (AR models) are a concept in time series analysis and forecasting that captures the relationship between an observation and several ...

2.1 Autoregressive Models | Stan User's Guide

https://mc-stan.org/docs/2_21/stan-users-guide/...

The simplest such model is the autoregressive conditional heteroscedasticity (ARCH) model Engle (1982). Unlike the autoregressive model AR(1), which modeled the ...

Autoregressive Model -- Properties of AR(1) Model

https://usmanr149.github.io/urmlblog/time%20ser...

30 апр. 2021 г. ... An autoregressive (AR) model predicts the future value based on previous values. Before jumping into the math behind AR models, we need to discuss a concept ...

A unified view of linear AR(1) models - Rob J Hyndman

https://robjhyndman.com/papers/ar1.pdf

For instance, any AR(1) model can be written in conditional distribution form by giving p(yt | yt−1), but this may be very complicated. For distributions which ...

What Are Autoregressive Models? How They Work and Example

https://www.investopedia.com/terms/a/autoregres...

An AR(1) autoregressive process is one in which the current value is based on the immediately preceding value, while an AR(2) process is one in which the ...

8.3 Autoregressive models | Forecasting - OTexts

https://otexts.com/fpp2/AR.html

Autoregressive models are remarkably flexible at handling a wide range of different time series patterns. The two series in Figure 8.5 show series from an AR(1) ...

🖼️ Изображения

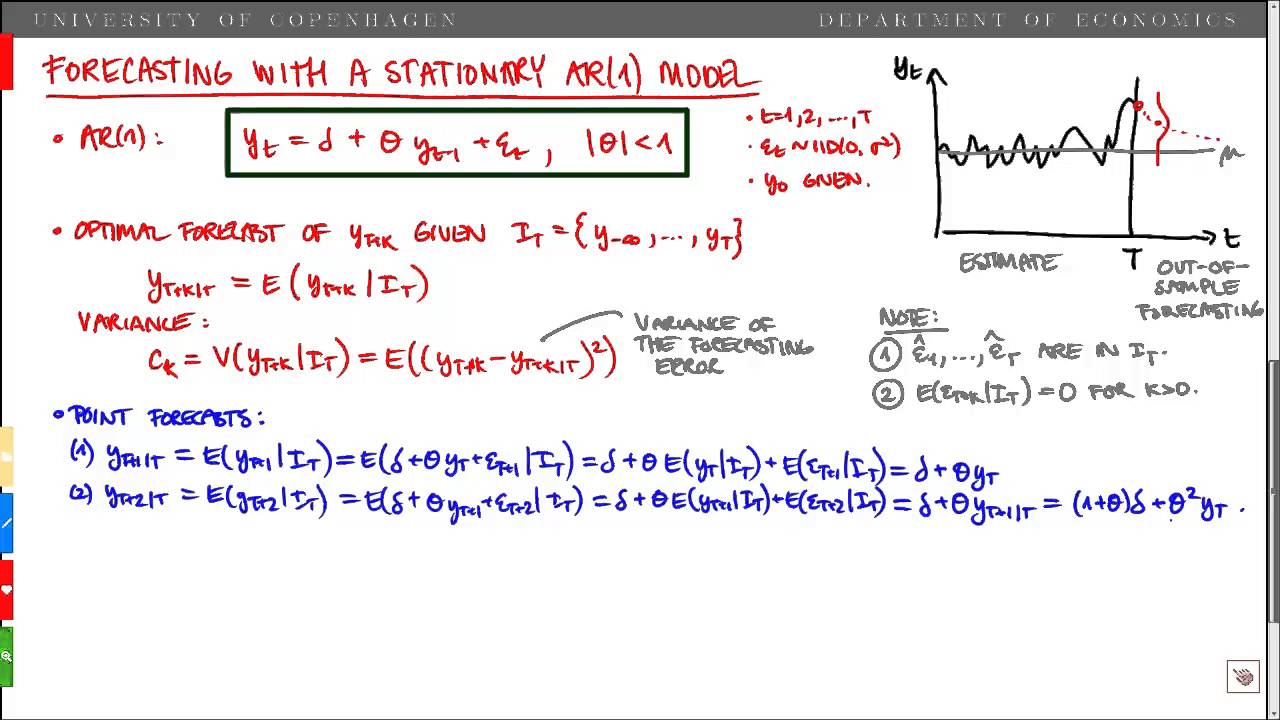

Forecasting With a Stationary AR(1) Model - YouTube

www.youtube.com

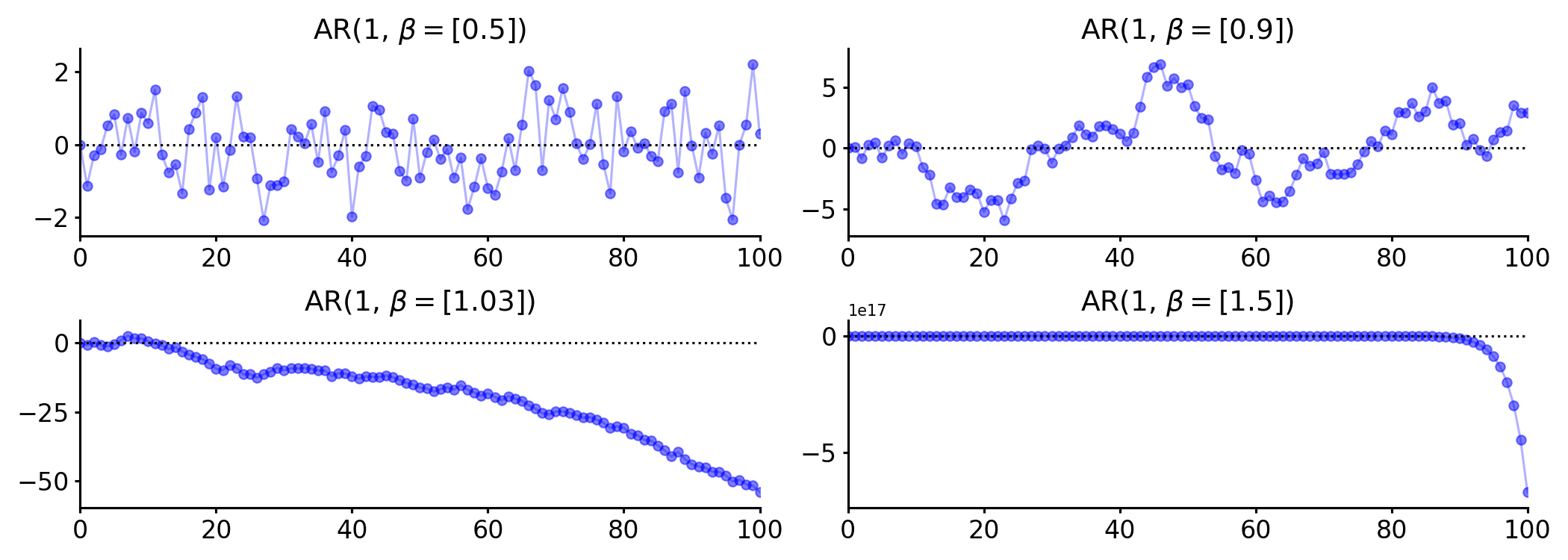

Example of AR(1) model graph | Download Scientific Diagram

www.researchgate.net

Autoregressive Model

gregorygundersen.com

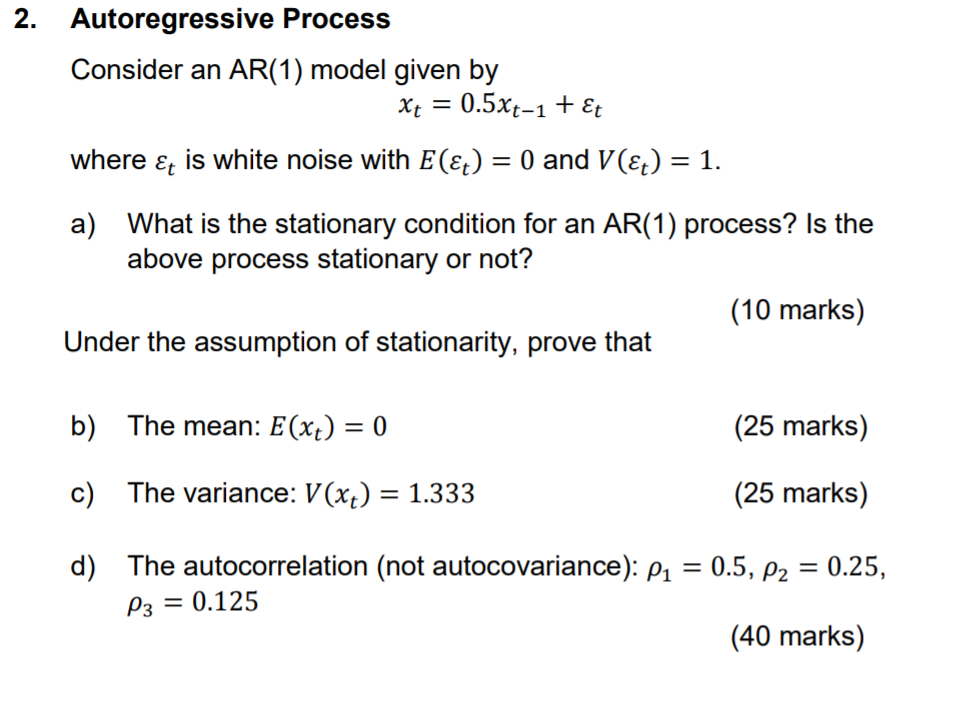

Solved 2. Autoregressive Process Consider an AR(1) model | Chegg.com

www.chegg.com

32: The graphs for the 1st individual to 10th individual with AR(1 ...

www.researchgate.net

The periodic response of a noise-free AR(1) model to sinusoidal forcing ...

www.researchgate.net

The AR(1) Model - Deriving the MA Representation by Recursive ...

www.youtube.com

+model+Where.jpg)

Regime Change and Convertible Arbitrage Risk - ppt download

slideplayer.com

Get Your Data On: Autoregressive Moving Average Models and Power ...

www.getyourdataon.com

🎥 Видео

The AR(1) Model - Stationarity Condition and Properties Given Stationarity

YouTube • October 21, 2015 • 09:35

We present the stationarity condition for the AR(1) model and derive the properties of the model given stationarity.

Maximum Likelihood Estimation of the AR(1) Model

YouTube • February 20, 2017 • 10:10

We derive the likelihood function for the AR(1) model.

AR(1) Process: Mean, Variance, Autocovariance and Autocorrelation function.

YouTube • October 12, 2016 • 09:48

Full derivation of Mean, Variance, Autocovariance and Autocorrelation function of an Autoregressive Process of order 1 (AR(1)). We firstly derive the MA infinity respresentation of a stationary AR(1). Usng this we can then derive the relevant properties.

Forecasting With a Stationary AR(1) Model

YouTube • October 27, 2015 • 09:18

We consider forecasting with a stationary AR(1) model. We derive the point forecasts and the variance of the forecasts one, two, and k periods ahead, and we show that these converge to the unconditional mean and variance, respectively, as the forecasting horizon goes to infinity.

The AR(1) Model - Deriving the MA Representation by Recursive Substitution

YouTube • October 21, 2015 • 06:36

We consider the AR(1) model and show how to derive the MA representation by recursive substitution.

OLS Estimation of the AR(1) Model

YouTube • February 20, 2017 • 07:44

We consider OLS estimation of the autoregressive parameter in the AR(1) model. Whenever the autoregressive paramter has true value between minus one and plus one, the OLS estimator is consistent.